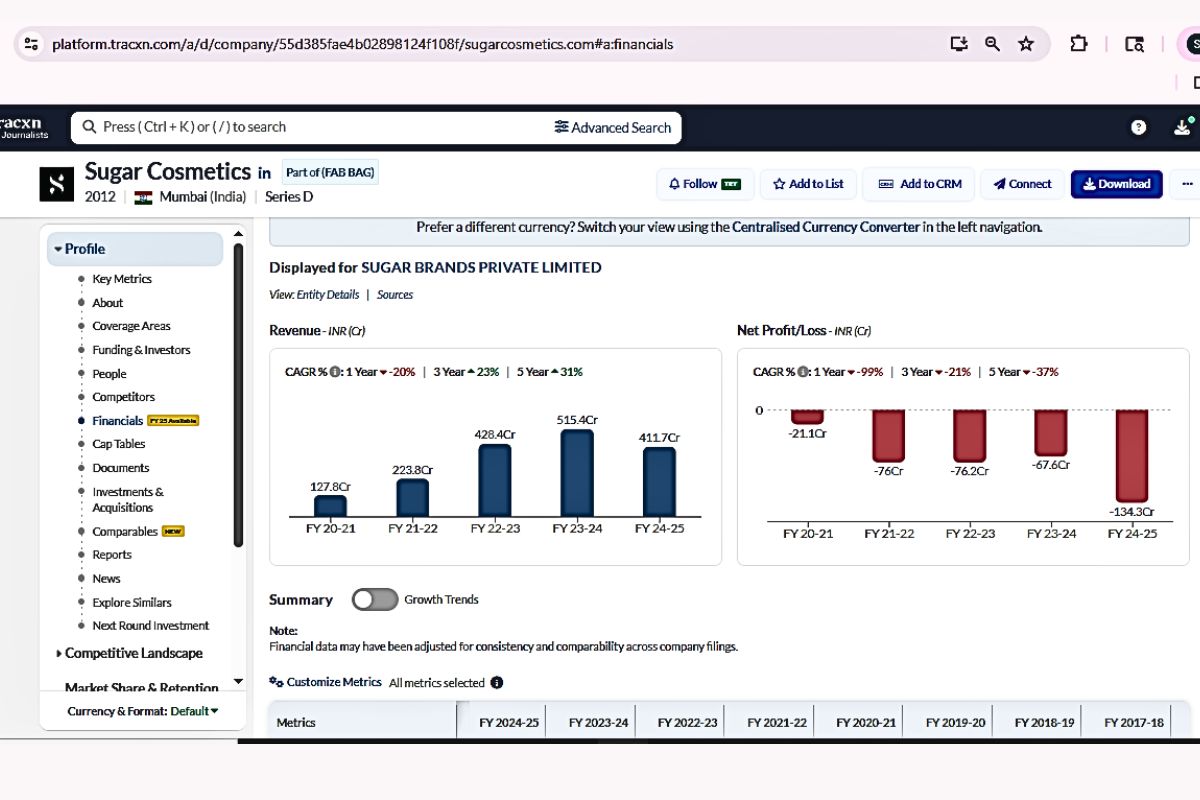

Sugar Cosmetics, a prominent Indian colour cosmetics brand, reported a net loss of ₹134.3 crore on revenue of ₹411.7 crore in FY2024-25, with losses nearly doubling from the previous year while revenue declined 20%. The deepening financial strain signals structural challenges in its D2C model, raising concerns for investors and supply-chain partners watching the Indian beauty market's trajectory toward $40 billion by 2030.

Financial trajectory and warning signs

Sugar Cosmetics' loss-to-revenue ratio reached 32.6% in FY25, far from the global benchmark of 8-12% positive net margin for scaled D2C beauty brands. In FY22, revenue nearly doubled to ₹223.8 crore, but losses tripled to ₹76 crore, a ratio of 34%. The company has not demonstrated profitable growth, with losses widening even as revenue contracted.

Cost structure and offline expansion burden

The brand expanded aggressively into 45,000+ retail touchpoints across 550+ cities post-pandemic. When incremental revenue from offline channels stalled, the fixed cost structure remained, eroding margins. Unlike leaner competitors, Sugar lacks manufacturing facilities, patented formulations, or exclusive retail relationships, making its cost base difficult to adjust.

Competitive landscape and commoditised differentiation

Sugar's early advantage—products formulated for Indian skin tones—is now widely replicated by Nykaa, Minimalist, Renee Cosmetics, and others. Nykaa's marketplace model generates gross margins without inventory risk, while Renee reached profitability faster with a leaner cost structure targeting tier-2 and tier-3 cities, the same markets Sugar is now retreating from.

What buyers should watch

For overseas distributors and clinic buyers evaluating Indian beauty brands, Sugar's case highlights the risk of brands without proprietary manufacturing or exclusive distribution. Its brand recall and founder equity require continuous reinvestment to maintain, and its high-quality cap table—including L Catterton, Elevation Capital, and A91 Partners—may face pressure to restructure. The Indian colour cosmetics market remains attractive, but supply-chain partners should prioritise brands with defensible production assets or unique channel access.

Source: Read the original report | Published: June 04, 2026