Hana Securities has identified 2026 as a pivotal year for K-beauty's global expansion, driven by widening export regions, entry into major offline retail chains, and category diversification. The report, published on June 9, offers strategic insights for overseas buyers and distributors eyeing structural growth beyond short-term trends.

Export shift: From China to Europe

K-beauty's export epicenter is moving rapidly. In 2024, China was the top destination; in 2025, the U.S. took the lead; and by Q1 2026, Europe surpassed the U.S. in export value, with year-on-year growth exceeding 50%. South Korea's total cosmetic exports reached $11.4 billion in 2025, making it the world's second-largest exporter, overtaking the U.S. and closing in on France within 4–5 years at the current pace. Within Europe, the U.K., Poland, and the Netherlands stand out. The U.K. is active both online and offline; Poland benefits from Silicon2's logistics center; and the Netherlands, via Rotterdam, serves as a distribution hub for northeastern Europe.

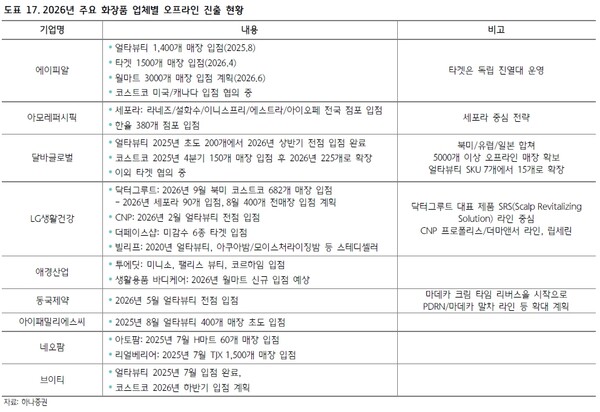

Offline channel breakthrough

After proving themselves on Amazon and other online platforms, K-beauty brands are now entering major global offline retailers. From 2026, listings at Ulta Beauty, Costco, Target, Walmart, and Boots are expected to ramp up. Given that over 85% of consumer spending in developed markets occurs offline, this shift is structural, not incremental.

Trade vendors like Silicon2, Grace, 222, and Most are playing a key role, handling logistics, inventory, pricing, marketing, and shelf management. As global retail networks expand, vendor networks become more critical than brand-only efforts.

Domestic channel diversification

In South Korea, the once Olive Young-centric channel structure is fragmenting. Daiso has emerged as a ultra-low-price beauty channel, generating an estimated 680 billion KRW (about 15% of its total 4.5 trillion KRW sales) from cosmetics in 2025, with roughly 500 SKUs and 60 brands. Pharmacies in tourist-heavy areas like Seongsu-dong, Hongdae, and Myeongdong are also becoming beauty retail points, with Dongkook Pharmaceutical's Centellian24, Madeca Pharma, and Hanmi Pharm's ProCam leading the trend.

Category growth: Hydrogel masks and inner beauty

Hydrogel mask exports surged 59% year-on-year in Q1 2026, with monthly growth of 86% in March and 88% in April. Brands like Biodance, Medicube, Anua, and Mediheal are driving demand. However, production is challenging due to high automation difficulty and yield management, with only 5–6 ODM suppliers—Jenix, Encore, Icare, Cosmax, Jincostech, and recently Cosmecca Korea—dominating supply. Inner beauty (functional foods for beauty) is the next growth frontier. U.S. buyers are increasingly interested, with exports to the U.S. up 58% in Q1 2026. Korean products leverage diverse formats like gummies, jellies, sticks, and capsules.

Fragrance: A rising category

Korean fragrance exports have grown at a 42% CAGR since 2020, exceeding $20 million for the first time in Q1 2026. Asia accounts for half of exports, but the U.S. is the top single-country market, with nearly 30% share.

Challenges: Japan, color cosmetics, and exclusivity

Japan, a key market for Korean color cosmetics due to similar skin tones, saw a 15% decline in May imports due to saturation and competition. Expanding color cosmetics in the U.S. and Europe is difficult because base makeup requires diverse shades—Sephora stores often stock over 20 shades per product, while Korean brands typically offer limited ranges (e.g., 19, 21, 23). This increases formulation, production, and inventory costs. Offline exclusivity agreements are also ending. Medicube's Ulta Beauty exclusivity expired in April 2026, and Laneige's North American Sephora exclusivity ends in late 2026. While this opens doors to more retailers, stable multi-channel performance remains to be verified.

Vendor competition and regional risks

Trade vendors are consolidating. Gudai Global acquired Hansung USA to strengthen its U.S. supply chain, while 222, Most, and Grace are rising. Direct market entry by large indie brands may widen performance gaps among vendors. New regions come with costs. Latin America is expected to gain traction by 2027, but security issues in Mexico require Grade-A warehousing and dedicated security. India's opaque distribution, grey markets, and administrative risks keep most players cautious. As global retail networks expand, local infrastructure investments may pressure vendor margins.

What buyers should watch

For overseas importers and distributors, the key signals are: (1) Europe's rapid emergence as a primary export region, especially the U.K., Poland, and the Netherlands; (2) the opening of major offline retail doors in the U.S. and Europe, which will require robust vendor partnerships; (3) the rise of hydrogel masks and inner beauty as high-growth categories with limited ODM capacity; and (4) the end of exclusivity deals, which may create new listing opportunities but also require careful channel management.

Source: Read the original report | Published: June 11, 2026