A new brand value ranking from Interbrand reveals a sharp split among South Korea's consumer goods brands in 2026, with channel- and category-specialized players like Olive Young and Daiso posting double-digit growth, while e-commerce leader Coupang and beauty giant LG Household & Health Care saw significant value erosion. For overseas buyers and distributors in medical aesthetics, the trend signals a shift toward specialized retail and away from generalist platforms.

Market signal

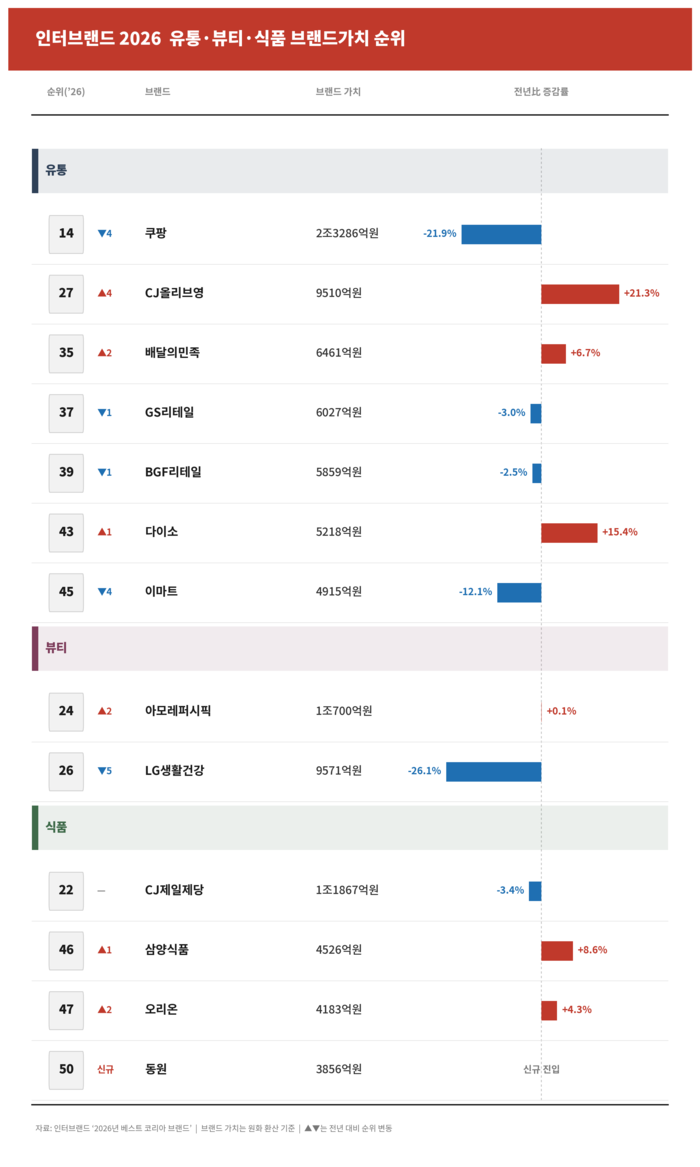

According to Interbrand's 2026 Best Korea Brands report, the total value of the top 50 Korean brands fell 1.6% year-on-year to KRW 231.1 trillion. The consultancy described 2026 as "the year of the gap," where brand value polarization intensified based on each company's ability to secure future growth engines and respond to market changes. This divergence was most evident in distribution, beauty, and food sectors.

Beauty and retail winners

CJ Olive Young jumped four spots to 27th place with a brand value of KRW 951 billion, up 21.3% year-on-year—the highest growth rate in the distribution category. Daiso, which expanded from value household goods into beauty and health functional foods, rose one spot to 43rd with KRW 521.8 billion, up 15.4%. Baedal Minjok (food delivery) also climbed two spots to 35th with KRW 646.1 billion.

Beauty and e-commerce losers

Coupang, the top e-commerce player, saw its brand value plunge 21.9% to KRW 2.33 trillion, dropping from 10th to 14th place amid customer data leaks, delivery worker rights controversies, and management response issues. LG Household & Health Care suffered the steepest decline among all brands, with value falling 26.1% to KRW 957.1 billion, sliding from 21st to 26th. Amorepacific edged up two spots to 24th with KRW 1.07 trillion, but growth was a mere 0.1%.

Sourcing context

For medical aesthetics buyers, the rise of specialized beauty retail channels like Olive Young and Daiso suggests growing consumer preference for curated, value-driven product discovery. Meanwhile, the decline of generalist e-commerce and large beauty conglomerates may indicate a shift in distribution power. Importers and distributors should monitor how these channel dynamics affect access to Korean beauty and aesthetic device brands.

What buyers should watch

The Interbrand analysis highlights that brands winning in 2026 are those offering concrete, trustworthy customer experiences and hyper-personalized engagement through data storytelling. For overseas buyers, this means Korean suppliers and retailers are increasingly prioritizing niche positioning and direct consumer relationships—factors that could influence partnership strategies, product selection, and channel negotiations in the medical aesthetics supply chain.

Source: Read the original report | Published: June 11, 2026