K-Beauty's indie brand boom is creating a stark performance divide within Kolmar Korea's supply chain. While the parent company's ODM business thrives on agile, small-batch production for indie brands, its packaging subsidiary Yonwoo struggles to shift from mass-production for large clients to the flexible, low-volume orders demanded by the indie segment. This transition is testing Kolmar's vertical integration strategy.

Market signal

South Korea's Ministry of SMEs and Startups reported that 2025 SME cosmetics exports reached $8.32 billion, up 21.5% year-on-year, a record high. SMEs accounted for 73.3% of total cosmetics exports in Q3 2025. In Q1 2026, SME cosmetics exports hit $2.18 billion, up 21.3% from the prior year, also a quarterly record. Indie brands are now the core driver of K-Beauty export growth.

Kolmar ODM gains from indie brand agility

Kolmar Korea was newly designated as a public-disclosure conglomerate by the Fair Trade Commission in 2026, with assets exceeding 5 trillion won, driven by K-Beauty demand. Its cosmetics ODM segment posted Q1 2026 revenue of 417.2 billion won, up 20.4% year-on-year, with an operating margin of 10.9%. The standalone entity's margin reached 14.9%. Indie brands favor ODM partners for fast product development and short launch cycles, benefiting Kolmar's model. An industry insider noted, "ODM companies that handle R&D, production, and quality control are gaining a competitive edge as indie brand exports expand. Kolmar is a direct beneficiary of this trend."

Yonwoo faces transition pains

Yonwoo, acquired by Kolmar in 2022, remains reliant on large clients: PKG Group, Amorepacific, and LG Household & Health Care accounted for 35.7% of its Q1 2026 revenue. Indie brands order smaller volumes with faster changeovers, but Yonwoo's cost structure—high fixed costs for molds and injection molding—requires scale for profitability. Combined with declining orders from major clients, its margins have suffered.

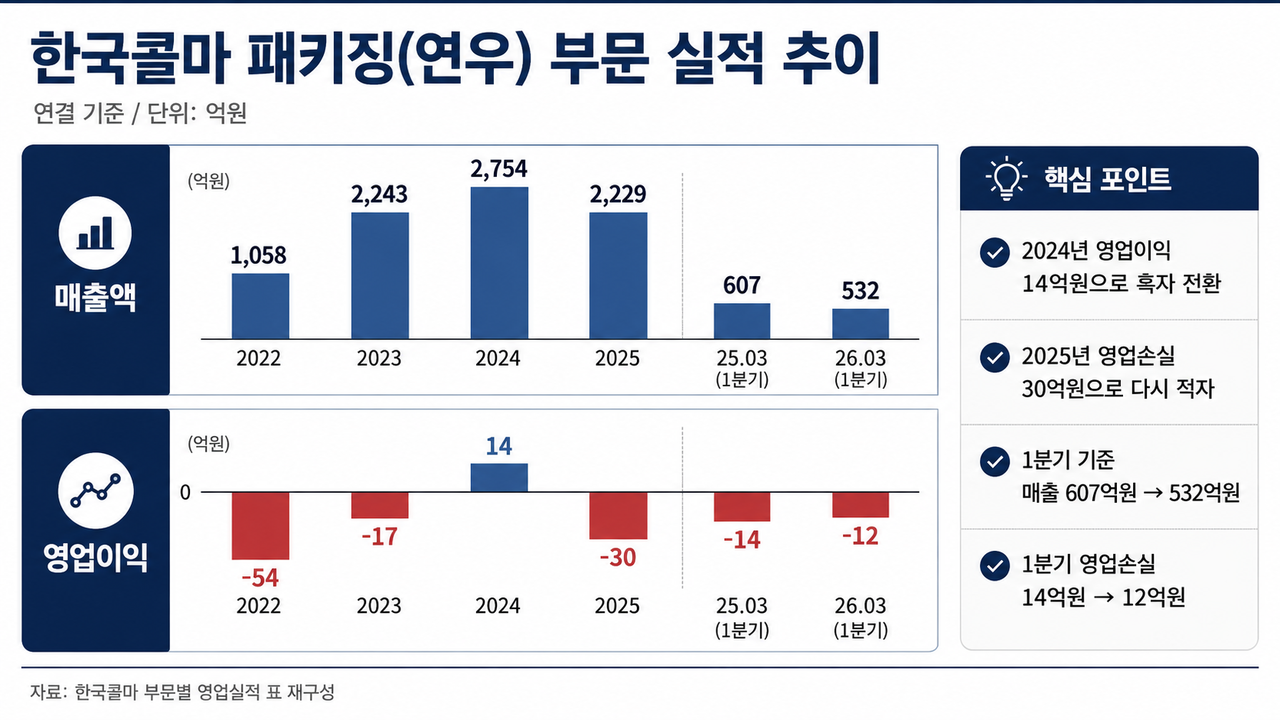

Financial impact on packaging unit

Yonwoo's consolidated revenue fell from 274.8 billion won in 2024 to 250 billion won in 2025, swinging from a 900 million won operating profit to a 300 million won loss. Kolmar's packaging segment overall saw revenue drop from 275.4 billion won to 222.9 billion won, with an operating loss of 3 billion won in 2025. In Q1 2026, the packaging unit reported 53.2 billion won in revenue and a 1.2 billion won operating loss.

What buyers should watch

For overseas distributors and clinic buyers sourcing K-Beauty products, Kolmar's ODM strength signals reliable, fast-turnaround manufacturing for indie brands. However, Yonwoo's packaging capacity constraints may affect lead times for customized containers. Buyers should monitor Yonwoo's progress in adapting to small-batch orders, as this will determine Kolmar's ability to offer seamless ODM-to-packaging vertical integration for indie brand clients.

Source: Read the original report | Published: June 11, 2026