South Korea's indemnity health insurance sector posted a loss of 1.87 trillion won in 2025, driven by rising claims for non-covered treatments such as manual therapy and non-covered injectables. This signals tighter regulatory scrutiny and potential cost-control measures that could affect medical aesthetics clinics and suppliers relying on non-covered procedures.

Losses and premium income

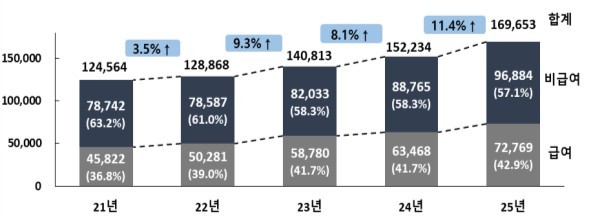

According to the Financial Supervisory Service's provisional 2025 business results released on April 3, the indemnity health insurance loss widened 15.6% year-on-year to 1.87 trillion won. Premium income rose 10.0% to 17.96 trillion won, driven by rate increases and new contracts, but claims paid grew faster at 11.4% to 16.97 trillion won.

Non-covered claims dominate

Non-covered claims accounted for 57.1% of total claims paid, reaching 9.69 trillion won. Among these, manual therapy and rehabilitation-related claims totaled 2.69 trillion won, exceeding cancer and cardiovascular disease claims (2.55 trillion won). Claims for non-covered outpatient injectables, including nutritional supplements, surged 31.9% to 1.04 trillion won.

New medical technology claims spike

Claims for new medical technologies rose sharply: robotic surgery claims jumped 72.4% to 470 billion won, prostate ligation 64.6% to 70 billion won, and HIFU procedures 46.0% to 220 billion won. These trends highlight growing utilization of advanced aesthetic and therapeutic procedures outside the national health insurance system.

Loss ratio and generational impact

The loss ratio worsened to 101.0%, up 1.7 percentage points from the previous year and well above the breakeven point of 85%. The third-generation product had the highest loss ratio at 120.3%, while the fourth-generation reached 115.1%. Older-generation policies showed higher per-contract claims: first-generation at 740,000 won, second-generation 490,000 won, third-generation 360,000 won, and fourth-generation 290,000 won.

Regulatory and channel signals

The FSS warned that continued loss deterioration could lead to further premium hikes and increased claim disputes. The newly launched fifth-generation product aims to curb excessive non-covered treatments. Starting July, fourth-generation policyholders will be guided to switch, and a new system for early adopters will launch in November. The regulator plans to monitor non-covered treatment usage and conduct on-site inspections of insurers with unfair claim practices.

What buyers should watch

For overseas distributors and clinic buyers supplying injectables, aesthetic devices, or consumables used in non-covered treatments, tighter cost controls in South Korea may reduce procedure volumes or shift demand toward covered alternatives. Suppliers should monitor regulatory changes and potential inclusion of certain non-covered treatments into the national insurance system, which could alter market dynamics.

Source: Read the original report | Published: June 03, 2026